- Download the Business Canvas Model sheet and fill it out for your fintech business idea. Share it in the forum if you like.

1 Like

Business Canvas Model of my project:

- Customer Segments : Man and women from 30 to 60 years old. On the full working age they often have the need to manage funds from different sources, for personal, familiar and working need. Check and manage the company account, a common account with partner, old parents account where they receive pension and social help, keep under control the bank activity of their your teenage sons, and some investment accounts for future pension, shares market and crypto currencies. The big number of different bank accounts, saving accounts and cryptocurrencies exchanges is creating confusion in the average user.

- Value Propositions : The added value at the basis of this project consists to manage all the personal, family, working finance on a single app. The user will have the possibility to easily interact not only on his personal account but also on all the third parties authorized accounts. The unified app will help the final user to manage as every external accounts he wants.

- Channels : Expecially at the beginning the online channels are to be preferred. All crypto currencies users are also bank account users and on big % investors, so they will highly feel the need of a unified app. So all the online channels for crypto currencies users are to be preferred.

- Customer Relationships : The way to be preferred is an online chat, kept by people working remotely

- Revenue Streams : First three-five synchronisations might be free. Then a small monthly fee might be added. An “opportunity advice” might be considered very useful from users about one suggested new fintech per week. This promotional space might be sold to generate a revenue

- Key Activities First step is the composition of the team. Then agreements with API aggregators and creation of the website and the apps. Then the public relationship activity.

-

Key Resources : A dynamic website

Android and iOS native apps

Remote customer service - Key Partnerships : Agreements with API aggregators Coinapi.io and Nordic API getaway. To be still identified: website company designer, apps designer, and customer relationship outsourcing.

- Cost Structure : Customer service is a recurring cost, as well a dedicated server. To be checked the contracts with API aggregators. Website and apps are one-time costs.

GUYS, WHO IS WILLING TO REALIZE THIS PROJECT WITH ME?

8 Likes

Cincinnato,

Good idea. Well fleshed out.

1 Like

Most middle-class citizens don’t know how to invest their savings properly or are too scared to do so because of past failures. My fintech would focus on making risk-free investing easy.

Value Propositions

We help customers earn ‘free’ money on their savings, as we will be only presenting offers through which our customers can only gain cash and not lose it. We will be comparing our services to deposits or savings account to show our customer that they have nothing to lose as they don’t earn any money on their savings currently. Our market advantages will be lowered risk and cost reduction, price, accessibility, and usability.

Customer Segments

Our end market will be all adults capable of using smartphones. But our ideal customers are middle-class higher educated city families actively thinking about their finance, freedom, and retirement.

Channels

Our customers most likely won’t trust, enjoy, or use technology freely outside of their career life. Network growth through offering a great product and affiliate benefits will be one of the channels for growth. It’s also worth keeping in mind that we will target middle-class people who often seek education and the latest news. Thus increasing awareness through online news outlets or LinkedIn may be an excellent place to advertise our services. We can also give out brochures outside of traditional banks and have booths during family festivals or events to explain how they can benefit and how our app works.

We will help customers evaluate our organizations’ value proposition by showing them our best available offers on our website.

Our service will be mostly used through Electron built desktop app or inside of a browser. Our customer base won’t be using phones as their preferred way of seeking financial help. Thus developing a good desktop solution will be our priority.

Customer Relationships

We will build a help center with videos explaining every detail of the service, but we will also allow our customers to contact us through emails and chat. And for the more significant users through the phone.

Revenue Streams

At the MVP level, the fintech would earn money by recommending certain bank’s services by aggregating the best risk-free investing offers into one app using APIs or inputting it manually. You would be able to register for any investment without leaving the app. The app would include offers such as earn up to 13% APY on Silver in the next two years, or we give you your money back. These kinds of offers are already popular, so I am sure they could be created or aggregated from other banks.

During the later developments of the app, different futures could be added, such as peer-to-peer lending. Anyone can register to receive a credit, but then we verify them, and then our customers can choose which people they want to lend money to, and we money-back guarantee their loans as does Mintos.

Key Resources

The company’s most valued resource will be our software and data. Followed by people that will be improving the software and making sure it follows all the regulations. And at last agreements with companies and permits.

Key Partners

We will have to raise money, so some of our partners will be shareholders providing financial support, as well as we may need to partner up with expert developers to develop responsive software. Besides that, we would need to partner with API aggregators and individual banks.

Key Activities

- Find a founding partner/pay for the developers.

- Create an MVP that would only compare other risk-free investments and choose the best ones for the customer.

- Raise money.

- Increase the team size, add customer support, and continuously improve the product.

Cost Structure

- Customer acquisition - most expensive

- Development

- Legal Work

- Server

- API costs

- Customer service - least expensive

In the link below, you can find a very helpful read I found while researching how to do the Business Canvas Model better:

8 Likes

Hope so! Thank you!

1 Like

-

People are renting homes on a yearly basis payment in the Middle East . most of the time the payment model is pretty unfair to the tenant. They will have to pay an amount of equivalent to 15 months of rental at once.

I am creating an app which people can list their properties and people whom are looking for a house can find places on the app.

Then the deposit amount which in most cases is over 3000 USD will be added to a liquidity pool. during the one year the deposit will make a return.

Once the duration is done then the profit will be shared between the owner and tenant, if the there any damages on the property then the owner can claim for damages and if the claim is correct the damage cost will be deducted from the deposit amount, otherwise it will be sent to the tenant. -

Online, websites, youtube, social media, influencers

-

everyone who is looking to rent a place

-

listing the property

-

Social media advertising through influencers

-

Marketing and development of the application in fact will have the highest cost

-

Investment opportunities, tenant and owner do not need to trust each other.

-

agents and developers. it is a more robust and fast way to find customers. also they can always monitor and track the house pricing.

-

investors, licensing, advisor, team

3 Likes

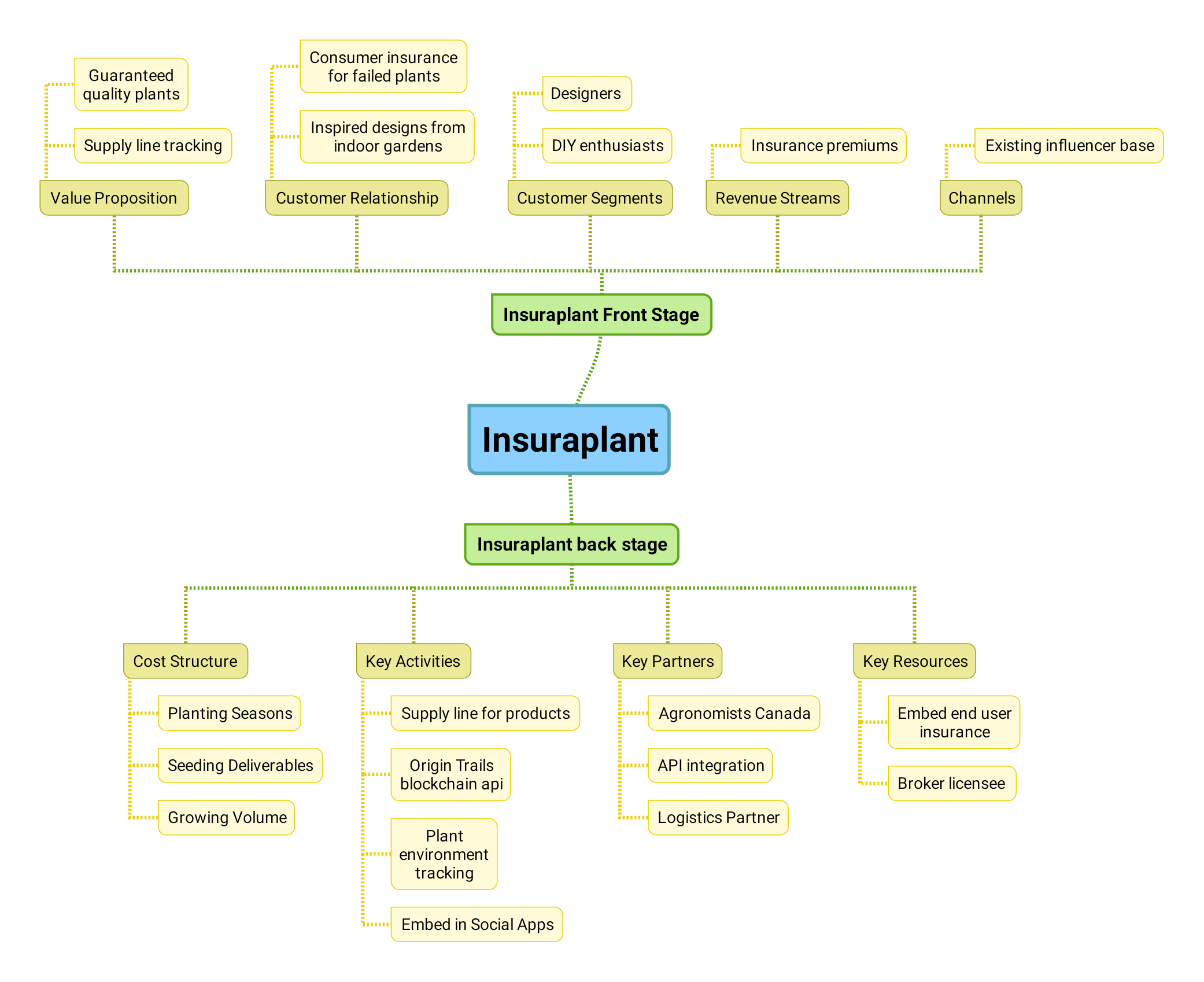

Good idea. Don’t forget seeds and gardening supplies! Grow tents, lights, timers, growing media, climate control, harvest equipment, nutrients, test tools. I’m a home gardener myself  You could also provide a service for helping obtain a licence for medical cannabis patients.

You could also provide a service for helping obtain a licence for medical cannabis patients.

1 Like

Hi

I can’t share this information publically

My Fintech proposition involves some established and less established players already in operation & so I cannot go into too much detail as I aim to realise it this year

Value Propositions

Build a Financial & Lifestyle super initially aimed at the underserved, more affluent Retail but also Coporate sector of the market but not exclusively so & generate enough “quality business” and AUM to expand the offering out to be one of global financial inclusion.

UN SDG focus & financial crime fighting edge to be incorporated

Core product stacks to include:

Payments, FX accounts & cards, REDACTED (use case), REDACTED (use case), Wealth app, income to bea earned through REDACTED (method)

REDACTED use case (requiring proprietary tech with on patrner in current dialogue)

Cyber-security & monitoring of global physical assets

Lifestyle convenience & benefits offerings

Educational services on financial literacy & wealth management

Customer Segments

Initially, high end HNW/UHNW and Corporate clients in the context of B2C, B2B

This will incorporate some B2B2C elements with Corporate customer branding, and powered by the new brand e.g. on Card offerings - use these offerings to onbard customers who wish to use the app

Boader customer base - generate revenues and profits through more profitable customers to build broader structures (requiring more costs) that will enable this offering to cater to a global market

Channels

Initial customer base will be affluent professionals, businesspeople, and mid-size to large coporates…

These people will be reached to scale initially through partbership to white label card services of existing B2C businesses with high value customer.

On boarding of Retail and Initial customers will focus on use of digital media (Adwords, Social Media acquisition channels, lead generation - & some key brand partnerships that have wide appeal)

Customer Relationships

Enable the highest quality of customer care, customer protection, customer choice & flexibility

Develop chat function that is monitored 24/7

Establish multi-lingual call centre in low-cost region to deal with unique cases

Revenue Streams

Payments & standard FX services will generate fees (full transparency to end user)

(REDACTED description) and asset conversion fees will be higher (full transparency to end user) & justified by unique propositions; other revenue services here to be rev-shared based, using BAAS integrated solutions

Ancillary fees through complementary / premium features including lifestyle & social elements (these will be from merchants and corporations, not from end users)

Key Resources

There is a great deal of proprietary tech already in place & this is a partnership route

The partnership strategy will establish relationships between medium-sized entities that will also incorporate services of 1 or 2 larger entities, that are all complementary

The combined resources there (IP, existing services, new technology that is being fine tuned) will keep development costs low… However there will still need to be additional developer resource & funds for marketing raised through public and also private means

Key Partners

Partners will need to be complementary such as to fulfill all of the above criteria (without naming them)

The likes of Refinitiv/Salv (for an edge in terms of proactive FinCEN activity) & likewise a Datia/Doconomy player (to lead in terms of SDG objectives & EU taxonomy compliance edge), all to be explored. Seek to incorporate lifestyle service providers within Super App (per AliPay & Tinkoff). Establish relationship with both traditional and crypto based API aggregators

Key Activities

Allow partners to use existing capital to scale existing products

Fund raise for new , innovate aspects of the offering under separate SBU

Run new activties as a speed boat initiative (engage digital marketing)

Incoporate new activities into pre-existing prodct services

Collate within one new super app…

Cost Structure

- Development & integrations of technologies

- New head of compliance with partner A

- Upgrade regulatory licensing

- API costs outsourced

- Customer acquisition through partners

- Digital marketing

4 Likes

- People are renting/buying property here in Malaysia . Sometimes the barrier to entry is rather steep as the deposit is usually 2.5months upfront. This is especially tough for people who were just starting to work as myself.

The app would be a P2P between the landlord and the tenant. Perhaps a decentralized way of tokenising property would work. Where one property can be bought by several people.

2. Online, websites, youtube, social media, influencers

3. Young adults/first time house buyers

4. listing the property

5. Social media advertising through influencers

6. Marketing and development of the application in fact will have the highest cost

7. Investment opportunities, tenant and owner do not need to trust each other.

8. agents and developers. it is a more robust and fast way to find customers. also they can always monitor and track the house pricing.

9. investors, licensing, advisor, team.

Inspired by

ghiasi12reza

3 Likes

nicely thought out tool n well presented - thnx!

1 Like

Great tool thanks. Done offline.

1 Like

First of all I want to thank you guys for your good ideas, here is my project:

Name of the Project: Grace Banking

1. Customer Segments : Our customer target consists of two groups. The first includes all low-income, high-debt people. The second group includes migrant groups such as Afro-Europeans.

We have brand ambassadors as a customer segment as a further component, as we want to train and coach the next generation of financial service partners with our e-learning academy.

2. Value Propositions: The added value on which this project is based is that we give people in financial difficulties the opportunity to participate in the global financial market despite all situations through our Grace Ecosystem. Migrants usually have a hard time making the right decisions about their finances, as in most cases there is a language barricade that leads to the fact that many are over-indebted or never have the opportunity to understand how and what money is. On our platform, our users will be able to get fixed interest on their assets, lower their effective interest rates by an average of 64% on existing installments, credit cards and personal loans and at the same time allow them to participate in projects such as DeFicake, Compound, Aave and many other DApps.

On the other hand, as a Grace Banking Ambassador, everyone has the chance to form communities on top of our Grace EcoSystem. For this there will be a unique commission model that enables everyone to be rewarded not only for the newly recruited users, but also for future customer relationships.

3. Channels : Like many other fintechs, Grace Banking will mainly be present online, which is why we are making our EcoSystem available primarily for our app, available for all smartphone models.

For our Ambassadors there will be a separate app that will enable them to receive all data in real time so that they can manage all of their customers and partners.

Furthermore we will help customers evaluate our organizations’ value proposition by showing them our best available offers on our website.

4. Customer Relationships : Establishment of 24/7 customer support - available in various foreign languages. In the first phase we want to establish and build ties with the Afro-European citizen. With the global financial education available to our clients through our app, we hope our clients can trust us and our Grace Ecosystem.

Through our ambassadors, we hope that they will use our Grace Ecosystem to create new, financially strong communities that use our products on a daily basis.

5. Revenue : Any winnings are paid out in our created currency (Coin of Grace). Furthermore, 30% of the interest and profits that our customers will achieve/gain with our ecosystem will flow back into the ecosystem.

Our ambassadors are paid entirely in our currency and 30% of their sales go back to the Grace ecosystem.

6. Key Activities : -Composition of the team & agreements with API aggregators -Web & App development -Raise money -Ambassadors training platform -Add customer support -Legal work(er)

7. Key Resources : Our most valuable resource is our app that gives access to our Grace ecosystem. Followed by our ambassadors promoting mass user adoption and creating communities that will use our Grace ecosystem.

8. Key Partnerships : In order to keep our Grace Banking App ecosystem stable, it is important that we only cooperate with the best DApps. I have listed a few here, but they have not yet been determined.

DApps

-Cakedefi Compound -Binance -Badger DAO

OpenBanking

-Fidor -openbankproject -adoriasoft

9. Cost Structure : - Development of website, app infrastructure and blockchain integration for our Grace Ecosystem (Coin of Grace) 20,000 €

-Legal Work 5,000 €

-Server 2,000 €

-API costs ~ 0 - <1,500 € per month

-Establishment of customer service 3,000 €

-E-learning platform 2,000 €

estimated cost: approx. 35,000 €

3 Likes

Amazing! Would love to see it happen one day.

2 Likes

-

Customer Segments - 18+, old and young, computer or mobile literate individuals mostly with an interest in sports and/or gambling and horse racing fans/enthusiasts in general.

-

Value Proposition - I offer a custom coded bot of my own making designed specifically for the ZED.run platform. The bot will operate the basic and advanced functions of a stable excluding the ability to withdraw funds to an external wallet. This means the bot will breed and race the horses in your stable, automatically sign up for all free races applicable to the horses class and rank, choose the best tracks location/length to suit the horses potential, so on and so forth. If you give permission the bot will place bets on your behalf as well. I can tell you that if there were such a thing people are already using it - even when only racing in free races you still win ETH.

-

Channels - Social Media engagement, email for direct contact, mobile push notifications and online advertising.

-

Customer Relationships - Same as channels with the addition of a 24/7 active help chat via discord, website, telegram group.

-

Revenue Streams - The bot may be rented out for flat fees dependent on the duration of use or may be used as a one off as well; again with a flat fee. An introductory rate may be used upon initial utilization. There could also be a lifetime use fee…

-

Key Activities - Coding/back testing bot, negotiating potential API w/ ZED.run platform, if not implementing a work around or separate UI for management and prompts/signals, telegram group.

-

Key Resources - telegram/discord, mobile support, software/dApp integration, remote customer service.

-

Key Partnerships - ZED.run #1 for sure, support from their end would be INVALUABLE, maybe a third party or just custom-built server run by a third party.

-

Cost Structure - Tech/customer service, server/electricity maintenance costs, perhaps some sort of kick back to ZED.run for API support or direct integration.

1 Like

INTRODUCTION.

Our project, called Domus, addresses the decrease of the residential real estate rent price, mortgagee’s installments as well as affordable housing gap challenging.

Mc Kinsey issued the Blue print in regards the last one.

https://www.mckinsey.com/~/media/McKinsey/Featured%20Insights/Urbanization/Tackling%20the%20worlds%20affordable%20housing%20challenge/MGI_Affordable_housing_Executive%20summary_October%202014.pdf . In their report the authors cite the following shocking figures:

Based on current trends in urban migration and income growth, we estimate that by

2025, about 440 million urban households around the world—at least 1.6 billion people—

would occupy crowded, inadequate, and unsafe housing or will be financially stretched.

The housing affordability gap is equivalent to $650 billion per year, or 1 percent of global

GDP. In some of the least affordable cities, the gap exceeds 10 percent of local GDP.

To replace today’s substandard housing and build additional units needed by 2025

would require an investment of $9 trillion to $11 trillion for construction; with land, the

total cost could be $16 trillion. Of this, $1 trillion to $3 trillion may have to come from

public funding.

Mc Kinsey researches comes to the conclusion that prices for a new development should be cut off by 20-50% to cover the gap. They identify four ways to reduce the cost of delivering affordable housing by 20 to 50 percent: unlock land at the right location (the most important lever), reduce construction costs through value engineering and industrial approaches, increase operations and maintenance efficiency, and reduce financing costs for buyers and developers.

Today we know that the above recipes don’t work. Moreover no one knows how increase of rent and secondary market property prices could be restrained.

We think in Domus that the decision could be find by virtue of fractioning of real estate to unlock a vast liquidity. For example, a digital fraction (or token) could be pegged by cm2 of physical real estate. The key issue why should the Domus token be better store of value than physical property? There are five underlying reasons:

-

Domus articulates a tokenisation of the evolution of real estate rather than a tokenisation of some property. It means that Domus generates the index token, which is fungible and exchangeable to the particular project token when these projects join to Domus. Projects are understood in a broad sense, i.e. development, housing association/REIT/landlord, mortgage REIT/mortgage broker. Therefore Domus approach covers letting, mortgage and development, all three pillars of real estate.

-

Domus Index Token (DIT) is a hybrid token, e.g. an asset token, a utility token and a payment token.

DIT is a “mercury” token which has two modes, i.e. utility(payment) mode and a security mode. It can exist only in one of these modes but can be switched between modes easily any given moment by token holder. -

Unified DIT is homegenising real estate of merged projects and it increases value.

-

Domus has a clear model of expansion by merging of new projects. New DITs are minted as new projects are absorbed and respectively DITs are burnt when the property is withdrawn from the Domus ecosystem.

-

Domus has own AMM ( automated market maker), which matches the growth of the ecosystem. We believe that the AMM cannot be defined once and for all. It depends on the amount of project joined and merged, time between merges, etc.

BUSINESS CANVAS MODEL

- Value proposition.

Unlocking of liquidity in residential real estate via tokenising of its fraction. A fair distribution of the difference between the token market price and underlying physical asset between landlords, mortgage suppliers and tenant and mortgagees, resulted an increase of revenue for asset holders as well as its capitalisation in comparison a routine way of business and a decrease of rent price and mortgage overpayment for tenants and mortgagees. A new store of value for retail investors as well as a new crypto asset for accredited and non-accredited traders, arbitrageurs and liquidity providers.

- Customer segment.

B2C: tenants, mortgagees, sole traders, LPs, arbitrageurs, retail investors, landlords.

B2B: different types of Housing Associations, mREITs, accredited and institutional investors.

3)Channels.

This is the main difficulty of the project. We need to approach first incumbents off-line and persuade them that they will have benefit. We will present our vision in some business schools and further try to use academical channels to establish contacts with PropTech people as well as different country’s real estate associations.

- Customer’s relationships.

B2C. Standard crypto project practice is setting up different online channels with community to listen ideas and complaints and to embed the best into the protocol. We like idea of governance tokens which are air dropping to encourage loyal stakeholders. We think that sooner or later the Domus holding company, which is responsible for consumer relations will shift towards the DAO model.

B2B. It is mostly routine off - line way of communications.

- Revenue streams.

Domus AMM is based on the uniquely designed TBC ( token bonding curve). A token can be sold only via TBC. If landlord, etc sales primarily the token he/she is liable to pay success fee between DIT market price and nominal price. Secondary long - term holders of token and traders will pay fee as well when they sell tokens. The amount of fee depends of different factors, for example, time of holding.

Tenants and mortgagees will pay a symbolic fee for the service access.

- Key resources.

Funding: FFF’s money, business angels.

Time: 2-3 years to deploy

Human resources: strong professional team ( some places are vacant)

- Key partners.

So far unclear.

- Key activities.

At this stage we need to obtain a pre-ruling from local EAA FMA in regards of token nature. Simply speaking it is a question of a legal feasibility of our project. Next crucial step is channels of distribution and a team framing.

GUYS I AM OPEN FOR DISCUSSION.

4 Likes

sounds like a nice idea. challenges are in the the backend where necessary links of various apps are so dynamic, the relevance of the apps you are using and probably the cost to the clients. that’s my two cents but otherwise it is an interesting proposition.